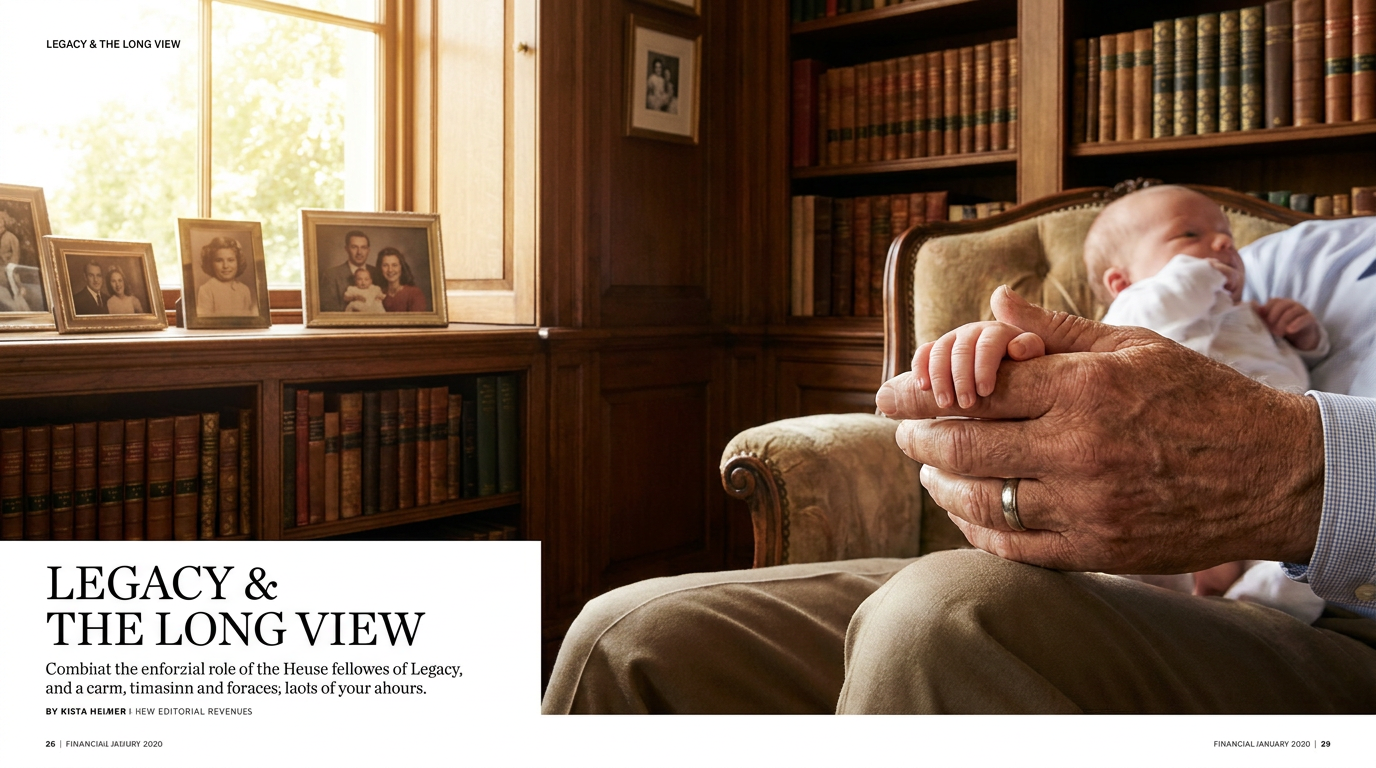

How to Fund a Child's Retirement From Birth: The New Rules of Generational Wealth

Recent legislative changes, including the SECURE 2.0 Act and a new birth-to-retirement pilot program, have created unprecedented tax-advantaged strategies for parents and grandparents to fund a child's retirement from day one.

By Factlen Editorial Team

- Financial Planners

- Emphasize the mathematical power of early compounding and the flexibility of the new SECURE 2.0 tax rules.

- Behavioral Risk Analysts

- Caution that transferring legal control of substantial retirement assets to 18-year-olds carries significant risk of premature withdrawal.

- Tax & Policy Experts

- Focus on the strict compliance rules, such as the 15-year holding period for 529s and the earned income requirements for rollovers.

What's not represented

- · Young Adults / Gen Z Beneficiaries

- · Low-Income Families Unable to Fund Accounts

Why this matters

By utilizing new legislative tools like the 529-to-Roth rollover and birth-to-retirement accounts, families can leverage decades of compound interest to permanently secure a child's financial future, bypassing the traditional model of late-in-life inheritances.

Key points

- The SECURE 2.0 Act allows up to $35,000 in unused 529 education funds to be rolled into a Roth IRA.

- A new pilot program for children born 2025-2028 seeds a retirement account with $1,000 and allows $5,000 annual contributions.

- Birth-to-retirement accounts bypass the standard IRS earned income requirement during the initial funding phase.

- Beneficiaries gain full legal control of birth-to-retirement accounts at age 18, introducing behavioral risks regarding early withdrawals.

Baby boomers currently hold an estimated $85 trillion in wealth, while millennials and Generation Z are burdened by unprecedented student loan debt and soaring housing costs. This generational disconnect has created a profound tension in American personal finance. Young adults are losing their most critical compounding years—their 20s and 30s—because their entry-level salaries are consumed by debt service.[1]

Historically, the advice from older generations was simply to "start saving early." But for a graduate dedicating $1,000 a month to student loans, funding a retirement account is often a mathematical impossibility. Recognizing this friction, grandparents and parents have increasingly sought ways to transfer wealth earlier in life, rather than leaving a lump-sum inheritance when the recipient is already in their 50s or 60s.[1]

Until recently, the tools available for early wealth transfer were heavily restricted. Trust funds are expensive to establish, and standard checking or brokerage accounts offer no tax shielding and are easily spent. However, a wave of recent legislative changes—most notably the SECURE 2.0 Act and a new pilot program for newborns—has fundamentally rewritten the rules of generational wealth.[5]

The most widely utilized new tool is the 529-to-Roth IRA rollover. For decades, 529 education savings plans have been the gold standard for college funding, allowing investments to grow tax-free if used for qualified educational expenses. But parents often hesitated to overfund these accounts, fearing that if a child earned a scholarship or chose a cheaper trade school, the leftover money would be trapped, subject to taxes and a 10% penalty upon withdrawal.[3][5]

The SECURE 2.0 Act, which took effect in 2024, eliminated that fear. Under the new rules, families can roll up to $35,000 of unused 529 funds directly into a Roth IRA in the beneficiary's name, completely tax-free and penalty-free. This allows a child who secures a scholarship to effectively convert their unused college fund into a massive head start on retirement.[2][4]

The rollover process is strictly regulated to prevent abuse. The 529 account must have been open for at least 15 years, ensuring the vehicle was genuinely intended for long-term savings. Furthermore, any contributions—and the earnings on those contributions—made within the last five years are ineligible for the transfer.[5][6]

Families also cannot move the entire $35,000 lifetime limit in a single transaction. The rollovers are subject to the IRS's annual Roth IRA contribution limits. In 2026, that limit is $7,500 for individuals under age 50. Therefore, maxing out the $35,000 lifetime allowance requires executing the rollover incrementally over a period of five years.[4][5]

Crucially, the beneficiary must have earned income equal to or greater than the rollover amount in the year the transfer occurs. If a recent graduate only earns $4,000 from a part-time job, the maximum 529-to-Roth rollover for that specific year is capped at $4,000, regardless of the broader $7,500 federal limit.[6]

While the 529 rollover solves the problem of leftover college funds, a more revolutionary change has quietly emerged for families welcoming new children. A new birth-to-retirement pilot program, active for children born between 2025 and 2028, allows families to bypass the standard rules of retirement accounts entirely.[1]

While the 529 rollover solves the problem of leftover college funds, a more revolutionary change has quietly emerged for families welcoming new children.

Under normal IRS regulations, an individual must have earned income to contribute to an IRA. This effectively prevents parents from opening retirement accounts for infants and toddlers. The new pilot program eliminates this barrier during the initial funding phase. The U.S. government seeds the account with a $1,000 initial deposit, and families are permitted to contribute up to $5,000 annually.[2][8]

The mathematical advantage of starting at birth is staggering. If a grandparent contributes the maximum $5,000 annually from the child's birth until age 18, they will have invested $90,000. Assuming a conservative 7% annual growth rate, the account could reach approximately $180,000 by the time the child graduates high school.[1]

At age 18, the structure of the account shifts. It is officially treated as a traditional IRA. The young adult can then choose to convert the balance into a Roth IRA. Because college students typically have minimal income, they fall into the lowest tax brackets (10% or 12%), making the conversion highly tax-efficient. Once converted, that $180,000 can compound entirely tax-free for the next 45 years.[2]

However, this unprecedented tax advantage comes with a significant behavioral catch: the transfer of control. At age 18 (or the age of majority in their state), the beneficiary gains full legal authority over the account. Grandparents may fund the account, but they cannot dictate how the money is used once the child reaches adulthood.[1][6]

This introduces a profound risk. While the funds are housed in a retirement structure, an 18-year-old could legally choose to liquidate the account. Doing so before age 59½ would trigger income taxes and a 10% early withdrawal penalty on the earnings, but the beneficiary could simply accept the penalty to access the cash for a car, a trip, or living expenses.[1]

For families uncomfortable with handing over control at 18, the traditional Custodial Roth IRA remains a powerful alternative, provided the child is old enough to work. If a teenager earns money from a summer job, babysitting, or lifeguarding, a parent or grandparent can open a Custodial Roth IRA and match their earnings, up to the $7,500 annual limit.[3][8]

The beauty of the Custodial Roth IRA is that the child does not have to deposit their actual paychecks. The grandparent can provide the funds for the contribution, allowing the teen to spend their summer earnings while still maxing out their retirement account. The only requirement is that the total contribution cannot exceed the child's reported earned income for the year.[3][8]

Navigating these accounts also requires a firm understanding of the IRS's "5-Year Rule." While original contributions to a Roth IRA can be withdrawn at any time without taxes or penalties, the earnings are heavily restricted. The account must be open for at least five tax years, and the owner must generally be 59½, before earnings can be withdrawn tax-free.[7][8]

There are exceptions to the penalty—such as withdrawing up to $10,000 for a first-time home purchase or using funds for qualified education expenses—but the income tax on earnings will still apply if the 5-year aging requirement is not met.[7]

Financial planners caution that while these generational wealth tools are powerful, they should never come at the expense of the older generation's financial security. Grandparents must ensure their own long-term care, healthcare expenses, and longevity risks are fully funded before locking capital into a grandchild's retirement account.[1]

Ultimately, the landscape of family finance has shifted. By moving away from the traditional model of late-in-life inheritances and embracing early-stage compounding, families now have the legislative tools to solve the retirement crisis for the next generation—provided they can instill the financial discipline required to keep the money invested.[6]

How we got here

Dec 2022

Congress passes the SECURE 2.0 Act, overhauling the U.S. retirement system and introducing the 529-to-Roth rollover provision.

Jan 2024

The SECURE 2.0 provision allowing up to $35,000 in unused 529 funds to be rolled into a Roth IRA officially takes effect.

Jan 2025

The new birth-to-retirement pilot program launches, providing a $1,000 government seed for eligible newborns.

2026

Annual Roth IRA contribution limits rise to $7,500, setting the maximum yearly pace for 529-to-Roth rollovers.

Viewpoints in depth

Financial Planners

Emphasize the mathematical power of early compounding and the flexibility of the new SECURE 2.0 tax rules.

Wealth managers argue that the traditional model of leaving an inheritance when the recipient is in their 50s or 60s is highly inefficient. By utilizing 529-to-Roth rollovers and the new birth-to-retirement accounts, families can leverage decades of tax-free compounding. Planners emphasize that even small contributions made during a child's first decade will mathematically dwarf much larger contributions made in their 30s, fundamentally solving the retirement crisis for the next generation.

Behavioral Risk Analysts

Caution that transferring legal control of substantial retirement assets to 18-year-olds carries significant risk of premature withdrawal.

Skeptics and behavioral economists point out a glaring flaw in the new birth-to-retirement accounts: the mandatory transfer of control at the age of majority. They warn that handing an 18-year-old legal authority over an account containing potentially $180,000 is a massive behavioral risk. Even with the deterrent of a 10% early withdrawal penalty and income taxes, the temptation to liquidate the funds for immediate lifestyle purchases—such as a car or travel—could easily override long-term retirement planning.

Tax & Policy Experts

Focus on the strict compliance rules, such as the 15-year holding period for 529s and the earned income requirements for rollovers.

Policy analysts stress that these new vehicles are not simple loopholes, but highly regulated tax structures requiring meticulous record-keeping. They highlight that the 15-year aging requirement for 529 rollovers prevents wealthy families from using education accounts as short-term tax shelters. Furthermore, they note that the requirement for the beneficiary to have earned income in the year of a 529-to-Roth rollover ensures the policy remains tethered to the traditional labor-based principles of the IRA system.

What we don't know

- Whether the 2025-2028 birth-to-retirement pilot program will be extended by Congress or allowed to expire.

- How the IRS will interpret edge cases regarding the 5-year contribution lookback rule for 529-to-Roth rollovers.

- What percentage of 18-year-olds will actually maintain the birth-to-retirement accounts rather than cashing them out and paying the penalty.

Key terms

- 529 Plan

- A tax-advantaged savings account designed to encourage saving for future education costs.

- Roth IRA

- An individual retirement account where contributions are made with after-tax dollars, allowing investments to grow tax-free and be withdrawn tax-free in retirement.

- SECURE 2.0 Act

- A major piece of U.S. retirement legislation passed in 2022 that introduced new rules, including the ability to roll unused 529 funds into a Roth IRA starting in 2024.

- Earned Income Requirement

- An IRS rule stating that an individual must have taxable compensation, such as wages from a job, to contribute to a standard IRA.

- 5-Year Rule

- An IRS regulation requiring a Roth IRA to be open for at least five tax years before earnings can be withdrawn tax-free.

Frequently asked

Can I roll over a 529 plan to a Roth IRA immediately?

No. The 529 account must have been open for at least 15 years, and the specific funds being rolled over must have been in the account for at least five years.

Does the child need a job to get the new birth-to-retirement account?

No. Unlike standard Roth IRAs, the new pilot program for children born between 2025 and 2028 bypasses the earned income requirement during the initial funding phase.

What happens to the birth-to-retirement account when the child turns 18?

It converts to a traditional IRA, and the 18-year-old gains full legal control. They can choose to convert it to a Roth IRA or even cash it out, though early withdrawals face taxes and penalties.

Does a 529-to-Roth rollover count against the annual IRA contribution limit?

Yes. The rollover amount counts toward the beneficiary's annual Roth IRA contribution limit, which is $7,500 in 2026.

Sources

Source coverage

8 outlets

3 viewpoints surfaced

[1]MarketWatchFinancial Planners

Fund a grandchild’s retirement tax-free from birth — if you can trust an 18-year-old with the money

Read on MarketWatch →[2]MorningstarBehavioral Risk Analysts

A new birth-to-retirement account bypasses standard Roth IRA rules

Read on Morningstar →[3]TIAAFinancial Planners

A more impactful financial gift: A Roth IRA

Read on TIAA →[4]Fidelity InvestmentsFinancial Planners

529 rollover to a Roth IRA: What to know

Read on Fidelity Investments →[5]Saving For CollegeTax & Policy Experts

529 to Roth IRA: Rollover Rules, Conversion Guide, and FAQs

Read on Saving For College →[6]Factlen Editorial TeamBehavioral Risk Analysts

Synthesis by Factlen editorial team

Read on Factlen Editorial Team →[7]Bankers LifeTax & Policy Experts

What Is the Roth IRA 5-Year Rule?

Read on Bankers Life →[8]Charles SchwabFinancial Planners

Roth IRA Withdrawal Rules

Read on Charles Schwab →

Every angle. Every day.

Get finance stories with full source coverage and perspective breakdowns delivered to your inbox.