The AI Memory Boom: Why Storage and Memory Stocks Are Surging

As artificial intelligence models grow exponentially larger, the industry's primary bottleneck has shifted from raw compute power to data transfer speeds, igniting a historic rally for memory manufacturers.

By Factlen Editorial Team

- AI Infrastructure Bulls

- Argue that the memory industry has undergone a structural transformation with permanent pricing power.

- Cyclical Skeptics

- Warn that the memory market remains vulnerable to historic boom-and-bust oversupply cycles.

- Hardware Engineers

- Focus on the physical limitations of silicon and the necessity of architectural breakthroughs.

What's not represented

- · Consumer Electronics Manufacturers

- · Smartphone Consumers

Why this matters

Understanding the shift from compute to memory is crucial for navigating the next phase of the AI boom, as the companies building the physical infrastructure of artificial intelligence see their business models fundamentally transformed.

Key points

- The AI industry's primary bottleneck has shifted from processing power (GPUs) to memory bandwidth.

- High Bandwidth Memory (HBM) solves this by stacking chips vertically, but it is highly complex to manufacture.

- Leading memory producers are entirely sold out of HBM capacity through the end of 2026.

- The focus on HBM has created a supply squeeze for traditional DRAM and storage, driving up prices across the sector.

- Memory stocks like Micron, SanDisk, and Western Digital have surged as the industry gains unprecedented pricing power.

For the past two years, the artificial intelligence investment narrative was dominated by a single component: the graphics processing unit. The world's largest tech companies raced to stockpile GPUs, treating raw compute power as the ultimate bottleneck in the AI arms race. But as those processors have grown exponentially faster, the bottleneck has shifted. The industry is now colliding with the "memory wall."

This shift has ignited a historic rally in a sector long dismissed as a low-margin commodity. Shares of memory and storage manufacturers like Micron Technology, SanDisk, and Western Digital have surged to record highs in 2026. Micron's market capitalization recently crossed the $1 trillion threshold, driven by a 57% year-over-year revenue surge to $13.64 billion in its latest quarter.[2][4]

The sudden repricing of these companies reflects a fundamental change in how AI systems are built. The artificial intelligence trade is no longer just about processing data; it is about moving and storing it. As AI transitions from experimental models to massive, real-world deployment, memory has become the critical infrastructure constraint.[3]

To understand why memory is suddenly so valuable, one must look at how large language models actually function. These models consist of billions, or even trillions, of parameters. During both training and inference—the process of generating a response—data must constantly shuttle between the memory chips where it is stored and the logic cores where the math is performed.[3][5]

For decades, processor speeds have advanced much faster than memory bandwidth. In modern AI workloads, moving the data back and forth now consumes significantly more time and energy than the actual calculations. If the processor is a massive factory, the memory interface is the single two-lane road leading to the loading dock. No matter how fast the factory works, it can only produce as much as the trucks can deliver.[3][5]

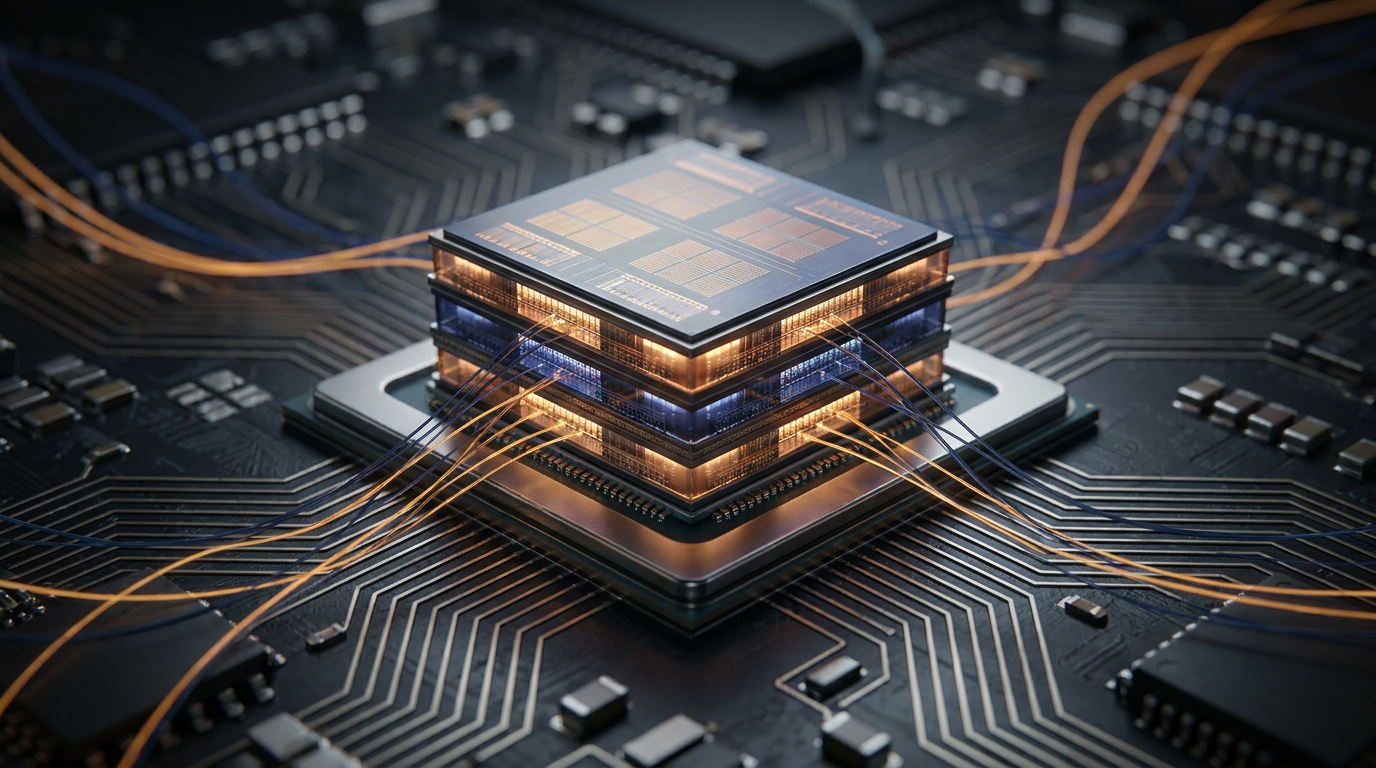

The solution to this traffic jam is a specialized technology called High Bandwidth Memory, or HBM. Unlike traditional memory chips that are laid out flat on a motherboard, HBM takes a vertical approach. Manufacturers stack multiple memory dies on top of one another—often 8 or 12 layers deep—and connect them using microscopic vertical channels known as through-silicon vias.[5]

This 3D-stacked architecture sits physically adjacent to the GPU on the same silicon package, drastically shortening the distance data must travel. The result is a massive expansion of the data highway. While traditional memory might offer bandwidth measured in gigabytes per second, the latest HBM4E modules can deliver over 4 terabytes of data per second per stack.[5]

But HBM is notoriously difficult to manufacture. The advanced packaging, precision stacking, and complex thermal management result in lower production yields compared to standard memory. Supply simply cannot be spun up overnight. As a result, the industry's leading HBM producers—SK Hynix, Micron, and Samsung—have reported that their high-bandwidth capacity is entirely sold out through the end of 2026.[4]

The advanced packaging, precision stacking, and complex thermal management result in lower production yields compared to standard memory.

This absolute supply constraint has handed memory manufacturers unprecedented pricing power. Long-term supply agreements and non-cancellable contracts have replaced the spot-market haggling that traditionally defined the memory business. Analysts project the total addressable market for HBM will reach $100 billion by 2028, fundamentally altering the profit margins of the companies that can produce it.[4]

The insatiable demand for HBM is also creating a massive ripple effect across the rest of the memory market. Because semiconductor fabrication plants have a finite capacity, manufacturers are aggressively reallocating their production lines away from standard DRAM to chase the higher margins of HBM.[6]

This reallocation has engineered a supply squeeze in traditional memory. With less standard DRAM being produced, prices for the memory used in everyday servers, personal computers, and smartphones are skyrocketing. Contract prices for conventional DRAM surged by an estimated 90% to 95% in the first quarter of 2026 alone.[6]

The AI boom is also driving a parallel surge in the need for persistent storage. While HBM and DRAM handle the active, real-time thinking of an AI model, the massive datasets used to train these models—and the outputs they generate—must be stored permanently. This requires vast arrays of NAND flash and high-capacity enterprise hard drives.[3][6]

Companies like SanDisk, which spun out as a pure-play NAND business, and Western Digital, which focuses on high-capacity data center storage, are riding this secondary wave. As hyperscalers build out massive new data centers, the demand for high-density enterprise solid-state drives has accelerated, lifting the entire storage complex alongside the memory makers.[3][6]

However, the sheer velocity of this rally has triggered warnings from some corners of Wall Street. Market analysts note that shares of Micron and SanDisk have pushed deep into "overbought" territory. The memory industry has historically been one of the most notoriously cyclical sectors in technology, defined by brutal boom-and-bust cycles.[1][6]

In past cycles, periods of high prices inevitably led to over-investment in new fabrication plants. Once that new capacity came online, supply would flood the market just as customer demand cooled, leading to a collapse in prices and profit margins. Skeptics warn that if hyperscalers suddenly pause their AI infrastructure spending, the current memory shortage could quickly turn into a glut.[1][6]

Yet, bulls argue that this time is structurally different. The capital intensity required to build modern HBM facilities is so high, and the technical barriers so steep, that new competitors cannot easily enter the market. Furthermore, the shift toward long-term, non-cancellable contracts provides a buffer against sudden demand shocks that didn't exist in previous cycles.[4]

The broader technology ecosystem is already feeling the impact of this shift. Rising memory costs are beginning to pressure the profit margins of consumer electronics manufacturers. Industry reports warn that if current trends hold, the smartphone and PC markets could face severe memory supply shortfalls by 2027, potentially driving up the cost of consumer devices.[7]

For now, the AI revolution remains fundamentally memory-bound. Until engineers discover a new paradigm for computing architecture, the speed of artificial intelligence will be dictated by how fast data can be retrieved from storage. In the infrastructure buildout of the 2020s, memory has evolved from a cheap commodity into the most valuable real estate in the data center.

How we got here

2023–2024

The AI industry focuses almost exclusively on acquiring GPUs, treating raw compute power as the primary bottleneck.

Early 2025

As AI models grow exponentially larger, engineers begin warning that data transfer speeds are throttling system performance.

Late 2025

Major memory manufacturers announce that their High Bandwidth Memory (HBM) capacity is fully sold out for the foreseeable future.

Spring 2026

A massive supply squeeze in both HBM and traditional DRAM drives contract prices up by over 90%, sending memory stocks to record valuations.

Viewpoints in depth

AI Infrastructure Bulls

Argue that the memory industry has undergone a structural transformation with permanent pricing power.

This camp, which includes specialized tech funds and semiconductor analysts, believes the historical boom-and-bust cycle of memory is dead. They point to the extreme technical difficulty of manufacturing High Bandwidth Memory and the shift toward long-term, non-cancellable contracts by hyperscalers. In their view, memory is no longer a cheap commodity but the foundational infrastructure of the AI era, justifying massive valuation premiums for companies that can successfully produce 3D-stacked chips.

Cyclical Skeptics

Warn that the memory market remains vulnerable to historic boom-and-bust oversupply cycles.

Skeptics caution that the current euphoria ignores the fundamental laws of semiconductor economics. They argue that the massive profit margins currently enjoyed by memory makers will inevitably lead to over-investment in new fabrication capacity. Once that capacity comes online—or if cloud providers suddenly pause their AI spending—the market could be flooded with excess supply, leading to a rapid collapse in prices. They point to technical indicators suggesting memory stocks are heavily overbought in the short term.

Hardware Engineers

Focus on the physical limitations of silicon and the necessity of architectural breakthroughs.

For chip architects and systems engineers, the financial rally is a secondary effect of a profound technical crisis: the Memory Wall. This camp emphasizes that raw compute power has scaled much faster than data transfer speeds. They argue that while HBM is a brilliant stopgap, the industry must eventually develop entirely new computing paradigms—such as processing-in-memory or optical interconnects—to prevent data movement from permanently throttling the advancement of artificial intelligence.

What we don't know

- Whether hyperscale cloud providers will maintain their current pace of infrastructure spending into the late 2020s.

- How quickly new fabrication plants can come online to alleviate the broader memory shortage.

- Whether emerging technologies like optical interconnects will eventually replace High Bandwidth Memory.

Key terms

- High Bandwidth Memory (HBM)

- A specialized type of computer memory that stacks chips vertically to drastically increase the speed at which data can be transferred to a processor.

- The Memory Wall

- A computing bottleneck where the processor's ability to perform calculations outpaces the speed at which data can be delivered from memory.

- Through-Silicon Via (TSV)

- Microscopic vertical electrical connections that pass directly through silicon dies, allowing stacked memory chips to communicate instantly.

- DRAM

- Dynamic Random Access Memory, the standard type of temporary working memory used in everything from personal computers to data center servers.

- NAND Flash

- A type of non-volatile storage technology that retains data even without power, commonly used in solid-state drives (SSDs) and smartphones.

Frequently asked

Why are memory stocks suddenly surging?

As artificial intelligence models grow larger, the bottleneck has shifted from processing power to data transfer speeds. Memory companies are seeing record profits because they supply the high-bandwidth chips required to keep AI systems running.

What makes High Bandwidth Memory different from normal memory?

Instead of laying chips flat on a motherboard, HBM stacks memory dies vertically and places them directly next to the processor. This 3D architecture allows for massive amounts of data to be transferred almost instantly.

Will this shortage affect consumer electronics?

Yes. Because manufacturers are dedicating their factories to producing high-margin AI memory, the supply of standard memory for PCs and smartphones is shrinking, which is driving up costs across the broader tech industry.

Is the memory chip industry still cyclical?

Historically, the memory market has experienced severe boom-and-bust cycles. While bulls argue that long-term AI contracts provide stability, skeptics warn that over-investment in new factories could eventually lead to an oversupply.

Sources

Source coverage

7 outlets

3 viewpoints surfaced

[1]MarketWatchCyclical Skeptics

Micron and Sandisk shares are phenomenally ‘overbought.’ Are memory stocks flying too close to the sun?

Read on MarketWatch →[2]Business InsiderAI Infrastructure Bulls

Micron and Memory Chip Stocks Fuel Rally to Records

Read on Business Insider →[3]Roundhill InvestmentsAI Infrastructure Bulls

The Memory Wall: Why AI's Next Bottleneck Isn't Compute

Read on Roundhill Investments →[4]IntrolAI Infrastructure Bulls

The AI Memory Supercycle: How HBM Became AI's Most Critical Bottleneck

Read on Introl →[5]RambusHardware Engineers

High Bandwidth Memory (HBM): Everything You Need to Know

Read on Rambus →[6]BBAECyclical Skeptics

Memory Stocks in 2026: What's Driving the Rally

Read on BBAE →[7]Factlen Editorial TeamHardware Engineers

Synthesis by Factlen editorial team

Read on Factlen Editorial Team →

More in finance

See all 5 stories →401(k) Trends

American 401(k) Balances Hit Record Highs as Auto-Enrollment Drives Savings Surge

0 sources

Stablecoin Adoption

Stablecoins Hit the Mainstream as Mastercard and Stripe Expand Global Blockchain Settlements

0 sources

Medical Debt Relief

The Yellow Envelope: How States Are Erasing Billions in Medical Debt in 2026

0 sources

Every angle. Every day.

Get finance stories with full source coverage and perspective breakdowns delivered to your inbox.