The Hidden Cost of EV Fender Benders: Why Insurance Premiums Are Up 42%

A minor collision in an electric vehicle can easily lead to a total loss due to the high cost of unrepairable battery packs. As insurance premiums surge, automakers and right-to-repair advocates are pushing for modular designs and diagnostic transparency to solve the crisis.

By Factlen Editorial Team

- Insurance Carriers

- Focuses on mitigating financial exposure and safety risks associated with compromised lithium-ion cells.

- Automakers & Manufacturers

- Prioritizes assembly efficiency and vehicle rigidity through integrated structural battery designs.

- Right-to-Repair Advocates

- Fights for diagnostic transparency and modular battery designs to reduce unnecessary waste and repair costs.

- Safety Researchers

- Tracks the long-term data on EV collision severity and the statistical trends of total loss declarations.

What's not represented

- · Independent Auto Body Shops

- · Salvage Yard Operators

Why this matters

Understanding the hidden insurance costs of electric vehicles allows buyers to accurately calculate their total cost of ownership. It also highlights the importance of shopping for specialized EV policies and supporting right-to-repair initiatives that could save thousands of dollars.

Key points

- EV insurance premiums now average 42% higher than comparable gas-powered cars due to elevated repair costs.

- Traction batteries account for up to 50% of an EV's value, making replacements prohibitively expensive.

- Without access to diagnostic data, insurers often total EVs after minor collisions to avoid battery fire liabilities.

- Automakers are shifting toward modular battery designs to allow targeted repairs and reduce total loss declarations.

The transition to electric vehicles has long been sold on a promise of long-term savings. While the sticker price might be higher, owners are told they will make it back by skipping oil changes, avoiding the gas pump, and relying on a drivetrain with a fraction of the moving parts of a combustion engine. But as EV adoption reaches critical mass in 2026, a hidden cost is shocking buyers and altering the total cost of ownership: surging auto insurance premiums. Across the United States, full-coverage insurance on an electric vehicle now averages roughly $3,500 to $4,000 per year, a staggering 42 percent higher than comparable gas-powered cars. For luxury and performance models, annual premiums can easily push into the five-figure range. This premium gap is not a penalty for going green, nor is it a reflection of driver safety. Instead, it is a direct mathematical response to a structural reality of electric vehicle design. Insurers are pricing in what happens when an EV gets into a collision, and they are finding that the very technology that makes the car electric also makes it financially perilous to repair.[2][3]

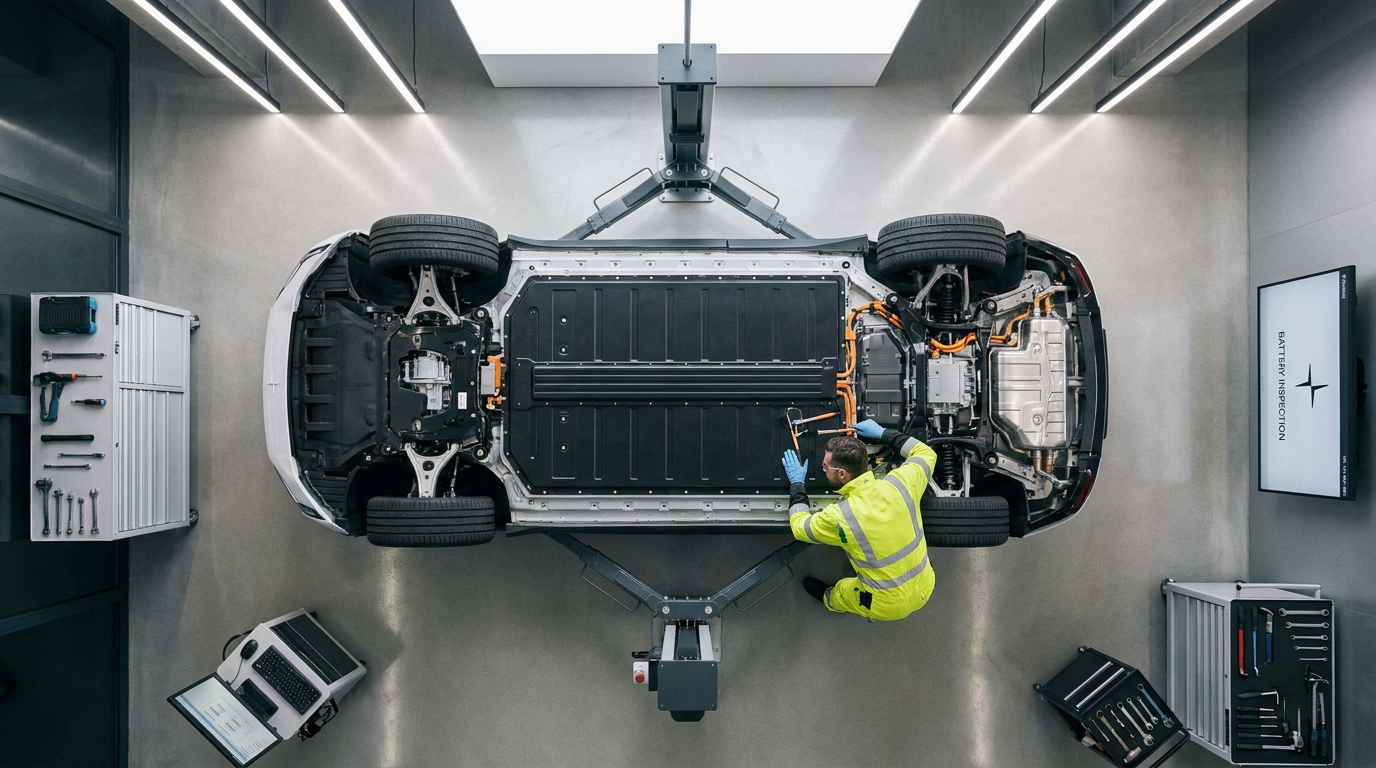

Every conversation about electric vehicle insurance inevitably starts and ends with the battery. In a traditional gas-powered car, the engine is expensive but highly repairable, and parts are widely available across a massive aftermarket network. More importantly, a routine fender bender almost never affects the engine block. In an electric vehicle, the architecture is fundamentally different. The traction battery pack is typically bolted directly to the underside of the vehicle, spanning the entire floorboard. This massive component represents the single most expensive part of the car, often accounting for 30 to 50 percent of the vehicle's total market value. Depending on the size, capacity, and manufacturer, a replacement battery pack can cost anywhere from $15,000 to over $22,000, before factoring in the specialized labor required to install it. Because of its location, the battery is highly vulnerable to underbody impacts, curb strikes, and side-impact collisions.[1][3][6]

When an electric vehicle is involved in a moderate collision, claims adjusters face a difficult and high-stakes decision. If the battery enclosure is dented, scratched, or punctured, there is often no immediate way to verify whether the lithium-ion cells inside have been compromised. A damaged cell is a severe fire risk, and insurers are unwilling to sign off on a repair that could result in a catastrophic thermal event weeks later. To know for sure, a technician must extract the battery and run extensive diagnostic tests. However, some automakers restrict access to the proprietary diagnostic data required to certify a battery as safe. Without the ability to definitively prove the pack is undamaged, the insurer must assume the worst and quote a full replacement.[1][4][8]

This diagnostic blind spot fundamentally alters the insurance math. Most insurance carriers operate with a "total loss threshold" set around 70 to 80 percent of a vehicle's depreciated actual cash value. If the estimated cost of repairs exceeds that threshold, the insurer declares the car a total loss, cuts a check to the owner, and sends the vehicle to a salvage yard. When a $15,000 battery replacement is added to the cost of standard bodywork, paint, and labor, the repair estimate almost instantly breaches that threshold. As a result, electric vehicles that look perfectly fine from the outside—perhaps suffering only a crumpled bumper and a scraped undercarriage—are routinely totaled. This high frequency of total loss payouts gets spread across the entire EV risk pool, driving up monthly premiums for every electric vehicle owner on the road.[3][5][6]

The problem is being exacerbated by a manufacturing trend that prioritizes assembly efficiency over long-term repairability. In a bid to lower production costs and increase vehicle rigidity, several major automakers, most notably Tesla, have transitioned to using "structural battery packs." In this design, the battery is not just a component bolted into the chassis; it is an integral, load-bearing part of the vehicle's physical structure. The cells are often glued into place with heavy-duty structural adhesives, making them virtually impossible to remove or service individually. While this innovation makes the cars cheaper and faster to build at the factory, automotive disassembly experts note that it results in "zero repairability" in the aftermarket. If a structural pack sustains even minor damage, the entire unit must be scrapped.[1][4][6]

The problem is being exacerbated by a manufacturing trend that prioritizes assembly efficiency over long-term repairability.

This dynamic is creating a paradox that undermines the environmental promise of the electric vehicle transition. The so-called "circular economy" of EVs relies on keeping cars on the road for hundreds of thousands of miles and eventually recycling their components. Instead, the high rate of total loss declarations is sending low-mileage electric vehicles straight to the grinder. Salvage yards are accumulating slightly damaged battery packs that cannot be legally reused in vehicles due to liability concerns and a lack of diagnostic transparency. While some of these batteries find second lives in stationary grid storage, the difficulty of processing and recycling them is producing far more automotive waste than early environmental models predicted.[4][6]

Beyond the battery itself, the electric vehicle repair ecosystem is struggling with a severe labor bottleneck. Repairing a high-voltage system requires specialized training, safety equipment, and dedicated bay space that most independent body shops simply do not have. The industry is currently facing a massive shortage of certified high-voltage technicians. Because demand for these specialized mechanics far outstrips supply, the shops that are equipped to handle EV repairs can charge significantly higher hourly labor rates. Furthermore, electric vehicles are often constructed with unique materials, such as lightweight aluminum and composite body panels, which require specialized adhesive bonding techniques rather than the traditional welding used on steel frames.[3][5][8]

Electric vehicles are also heavily reliant on advanced driver-assistance systems (ADAS), which add another layer of cost to every repair. The bumpers, fenders, windshields, and grilles of modern EVs are packed with ultrasonic sensors, radar units, and high-definition cameras. Even in a minor collision that does not damage the battery, these delicate sensors are frequently destroyed. Replacing the hardware is expensive, but the true cost lies in the software recalibration required to ensure features like lane-keeping assist and adaptive cruise control function safely. This recalibration process can easily add $1,000 or more to a standard bodywork bill, further inflating the average claim severity for electric vehicles compared to their analog predecessors.[3][5]

Despite these challenges, the automotive and insurance industries are actively working to adapt and solve the EV repair crisis. Recognizing that uninsurable cars will eventually deter buyers, legacy automakers like Ford and General Motors are pivoting away from monolithic structural packs. Instead, they are designing modular battery architectures. In a modular system, the battery pack is divided into distinct, replaceable cell modules. If a specific section of the battery is damaged in a crash, a technician can swap out just the affected module for a fraction of the cost of a full pack replacement. This shift toward repairability is expected to drastically reduce the number of total loss declarations triggered by minor underbody impacts.[1][6]

Simultaneously, a fierce legislative battle is unfolding over diagnostic transparency. Right-to-repair advocates are pushing state and federal lawmakers to mandate that automakers share battery diagnostic data with independent repair shops and insurance adjusters. If an independent technician can plug into an EV and definitively verify that the internal cells are healthy after a collision, insurers will no longer have to default to expensive replacements. Several states are currently drafting legislation that would require manufacturers to provide standardized access to battery health metrics, a move that advocates argue is essential for creating a competitive, affordable repair market.[1][4]

Insurance carriers are also evolving their business models to better accommodate the unique risk profile of electric vehicles. Rather than relying on broad-stroke actuarial tables that penalize all EVs, forward-thinking insurers are leveraging telematics to offer personalized rates. Because electric vehicles are essentially rolling computers, they can seamlessly transmit driving data—such as acceleration habits, braking severity, and average speeds—directly to the insurer. Drivers who operate their EVs conservatively can unlock significant discounts that offset the higher baseline premiums. Additionally, some carriers are introducing EV-specific policy add-ons, such as coverage for charging cables, wallbox damage, and specialized towing to functional charging stations.[3][8]

While the current landscape presents a financial shock to many new electric vehicle owners, industry analysts expect the premium gap to narrow significantly in the coming years. As battery production scales globally, the raw cost of replacement packs is steadily declining. At the same time, the aftermarket repair network is slowly catching up, with more independent shops investing in high-voltage training and equipment. As insurers accumulate more granular data on EV collision outcomes, their pricing models will become more precise, reducing the uncertainty premium currently baked into the rates. For now, consumer advocates advise EV buyers to shop their insurance policies aggressively, as rates for the exact same vehicle can vary by thousands of dollars between carriers.[2][3][7]

How we got here

2020

Early data from the Highway Loss Data Institute reveals that average total loss payments for EVs are significantly higher than for conventional vehicles.

2022

Automakers increasingly adopt structural battery packs to reduce manufacturing costs, inadvertently complicating aftermarket repairs.

2024

Reports emerge of low-mileage EVs being scrapped over minor battery scratches, highlighting the lack of diagnostic transparency.

2026

EV insurance premiums reach an average 42% premium over gas cars, prompting a push for modular battery designs and right-to-repair legislation.

Viewpoints in depth

The Automakers' View

Prioritizing manufacturing efficiency and vehicle performance.

For manufacturers, integrating the battery directly into the chassis as a structural component is a massive leap in engineering efficiency. It reduces the overall weight of the vehicle, increases structural rigidity, and significantly lowers the cost of assembly at the factory. Automakers argue that these upfront savings make electric vehicles more accessible to the average consumer, even if it complicates aftermarket repairs. Furthermore, restricting third-party access to battery diagnostics is often framed as a safety measure to prevent untrained mechanics from mishandling high-voltage systems.

The Insurers' View

Managing the financial and safety risks of compromised lithium-ion cells.

Insurance carriers are fundamentally risk-averse, and a compromised lithium-ion battery represents an unacceptable liability. If an insurer signs off on a repair and the battery later catches fire, the financial and reputational damage is catastrophic. Without standardized, transparent diagnostic data from the manufacturer proving the internal cells are pristine, adjusters have no choice but to assume the pack is dangerous. The math is simple: when a $20,000 battery replacement pushes the repair bill past the vehicle's total loss threshold, totaling the car is the only mathematically sound decision, even if it drives up premiums for the entire risk pool.

The Right-to-Repair View

Fighting for diagnostic transparency and sustainable repair practices.

Right-to-repair advocates view the current situation as an artificial crisis created by corporate monopolies. They argue that automakers are intentionally locking independent mechanics out of the diagnostic software needed to verify battery health, forcing consumers back to expensive dealerships or resulting in unnecessary total losses. By pushing for legislation that mandates open access to diagnostic codes and encouraging the adoption of modular battery designs, these advocates aim to break the monopoly, lower insurance premiums, and stop the environmental waste of sending perfectly good batteries to the scrapyard.

What we don't know

- How quickly independent repair shops will be able to scale their high-voltage certification to meet growing demand.

- Whether upcoming right-to-repair legislation will successfully force automakers to share proprietary battery diagnostic data.

Key terms

- Traction Battery

- The large, high-voltage lithium-ion battery pack that provides power to the electric motors to propel an EV.

- Total Loss Threshold

- The percentage of a vehicle's value (usually 70-80%) at which an insurer decides it is cheaper to scrap the car than pay for repairs.

- Structural Battery

- A manufacturing design where the battery pack is integrated into the vehicle's frame as a load-bearing component, making it difficult to remove or repair.

- Telematics

- Technology that transmits real-time driving data (like speed and braking habits) to insurers, often used to calculate personalized insurance discounts.

Frequently asked

Does my standard car insurance cover EV battery damage?

Yes, comprehensive and collision policies generally cover battery damage from accidents. However, if the replacement cost exceeds the vehicle's total loss threshold, the insurer will total the car rather than repair it.

Why can't a damaged EV battery just be repaired?

Many modern EVs use sealed or 'structural' battery packs that are glued together. Without access to proprietary diagnostic data, repair shops cannot verify if the internal cells are safe from fire risks, forcing a full replacement.

Are EV insurance premiums expected to drop?

Industry analysts expect premiums to stabilize as battery production costs fall, more independent mechanics get high-voltage certification, and automakers shift toward repairable, modular battery designs.

What is a structural battery pack?

It is a battery design where the pack acts as a load-bearing part of the car's chassis. While it makes manufacturing cheaper and the car lighter, it makes the battery nearly impossible to repair after a crash.

Sources

Source coverage

8 outlets

4 viewpoints surfaced

[1]ReutersAutomakers & Manufacturers

Scratched EV battery? Your insurer may have to junk the whole car

Read on Reuters →[2]InsurifyInsurance Carriers

Electric vehicle insurance costs up 42%

Read on Insurify →[3]RoadEthosInsurance Carriers

In 2026, EV Insurance Premiums Surge as Batteries Turn Fender Benders Into Total Losses

Read on RoadEthos →[4]Motor.comAutomakers & Manufacturers

Slightly damaged electric vehicle batteries translate into dead ends

Read on Motor.com →[5]Claims JournalInsurance Carriers

Understanding the Reality of EV Insurance Costs

Read on Claims Journal →[6]JalopnikRight-to-Repair Advocates

Minor Crashes Are Totaling EVs Because The Batteries Are Too Expensive To Fix

Read on Jalopnik →[7]Highway Loss Data InstituteSafety Researchers

Average payments for total losses for EVs are higher than conventional vehicles

Read on Highway Loss Data Institute →[8]Starwest InsuranceInsurance Carriers

3 Reasons Your Tesla Premium Just Spiked

Read on Starwest Insurance →

Every angle. Every day.

Get automotive stories with full source coverage and perspective breakdowns delivered to your inbox.