The Hidden 'Index Machine' Forcing Billions Into SpaceX Stock

SpaceX's record-breaking IPO triggered a race among index providers to rewrite their rules, forcing passive funds to automatically buy billions of dollars in shares.

How this story has developed

This report is part of a developing story — read the earlier chapters below.

- SpaceX Targets $1.8 Trillion Valuation for IPO, Down from $2 Trillion

- The SpaceX IPO Explained: How Starlink and Reusable Rockets Built a Public Market Giant

- S&P 500 Crosses 7,600 as AI Infrastructure Boom and SpaceX IPO Fuel Historic Market Rally

- Australian Mining Giant Hancock Prospecting Secures $1 Billion Stake in SpaceX Following Record IPO

- SpaceX to Acquire AI Coding Startup Cursor for $60 Billion in Major Enterprise Push

- SpaceX Surpasses Amazon in $2.8 Trillion Valuation Surge Following $60 Billion Cursor Acquisition

- SpaceX Acquires AI Code Editor Cursor for $60 Billion in Landmark Tech Deal

- The Index Effect: Why Your Vanguard Fund Is Buying SpaceX, But Your S&P 500 Fund Isn't

- SpaceX Acquires AI Startup Cursor for $60 Billion Days After Record $75 Billion IPO

- The Hidden 'Index Machine' Forcing Billions Into SpaceX Stock (this article)

- SpaceX's IPO Triggers a Passive Investing Tug-of-War Over Index Inclusion

- SpaceX Acquires AI Coding Startup Anysphere for $60 Billion in All-Stock Blockbuster Deal

- The Mechanics of the Mega-Merger: How SpaceX's $250 Billion xAI Acquisition Creates a Space-Based AI Infrastructure

- The Mechanics of the Historic IPO: How SpaceX Raised $85.7 Billion in Its Landmark Nasdaq Debut

- SpaceX and xAI Combine in $113 Billion Deal, Rolling X Into New AI Infrastructure Giant

- SpaceX Completes Largest IPO in History, Debuting on Nasdaq at $2 Trillion Valuation

- SpaceX Agrees to Acquire xAI for $250 Billion in Largest M&A Deal in History

- SpaceX Completes Record $1.75 Trillion IPO, Signaling New Era for AI Mega-Caps

- SpaceX Stock Drops 7% on First Post-IPO Earnings as AI Capital Expenditure Surges

- Is the Senate's Inaction on ACA Subsidies a Deliberate Strategy to Dismantle the Affordable Care Act?

- Passive Index Providers

- Advocates for fast-tracking mega-cap IPOs into market benchmarks.

- Traditional Benchmark Defenders

- Proponents of strict seasoning and profitability rules for index inclusion.

- Market Structure Analysts

- Experts focused on the mechanical plumbing of stock market liquidity.

How we got here

May 20, 2026

SpaceX files its S-1 prospectus, declaring plans for a massive public listing.

June 4, 2026

S&P Global announces it will not alter its rules, blocking SpaceX from early S&P 500 entry.

June 12, 2026

SpaceX completes the largest IPO in history, raising $75 billion at a $1.77 trillion valuation.

June 18, 2026

SpaceX is added to the CRSP and FTSE Russell indices, triggering billions in passive buying.

Why it matters

Millions of everyday investors now automatically own a piece of SpaceX through their retirement accounts and passive ETFs, even if they never actively bought the stock. Understanding how index inclusion forces these purchases reveals the hidden mechanical plumbing that drives modern stock market valuations.

When Space Exploration Technologies Corp. went public on June 12, 2026, it shattered every record on Wall Street. Pricing at $135 per share, the SpaceX initial public offering raised $75 billion and debuted with a staggering valuation of $1.77 trillion. Retail investors immediately flooded the zone, driving the stock up 67% at its intraday peak as the market scrambled to own a piece of Elon Musk's aerospace giant.[1][2][4]

But as the initial retail frenzy began to cool—with shares settling to roughly 33% above their IPO price by the end of the first week—a second, much larger wave of capital was quietly preparing to strike. This incoming tide of cash is not driven by human emotion, fear of missing out, or fundamental analysis. Instead, it is the result of mechanical, price-insensitive algorithms known as the "index machine."[1][6]

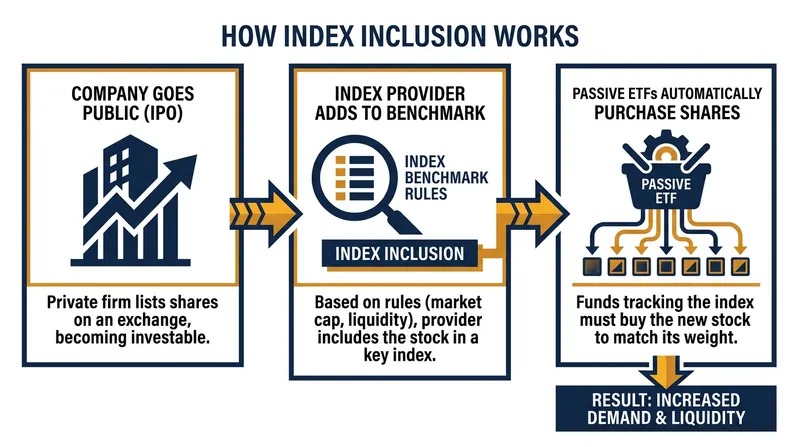

To understand this hidden market force, investors must look at the mechanics of index inclusion. When a company is added to a major stock benchmark like the Nasdaq-100 or the Russell 1000, every passive mutual fund and exchange-traded fund (ETF) that tracks that index is legally obligated to buy the stock.[3]

These passive funds do not care about a company's valuation multiples, its future earnings potential, or the latest headlines. If a stock represents 1% of the underlying index, the fund manager must allocate exactly 1% of their portfolio to that stock to ensure accurate replication.[6]

Historically, companies have had to wait months or even years to join these exclusive benchmark clubs, proving their stability over time. But SpaceX's sheer size broke the traditional system. At nearly $2 trillion, excluding the aerospace company would make broad market indexes fundamentally inaccurate representations of the U.S. economy.[3]

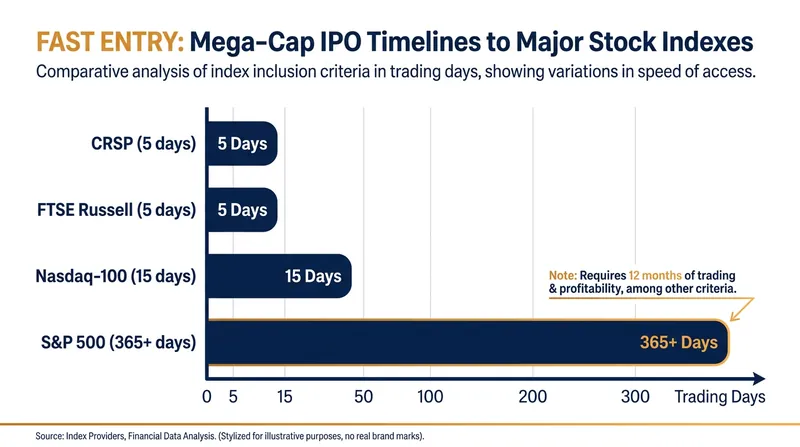

Faced with the largest IPO in history, major index providers scrambled to rewrite their rulebooks. The Center for Research in Security Prices (CRSP) and FTSE Russell instituted "Fast Entry" rules specifically designed for mega-cap listings, allowing massive companies to join their indexes after just five trading days.[2]

Nasdaq quickly followed suit. The exchange updated its methodology to allow entry into the tech-heavy Nasdaq-100 index after 15 trading days. Crucially, Nasdaq also eliminated its strict 10% minimum float requirement, a rule that would have otherwise disqualified SpaceX from early inclusion.[3]

The exchange updated its methodology to allow entry into the tech-heavy Nasdaq-100 index after 15 trading days.

These accelerated timelines triggered a massive, synchronized liquidity event. On June 18, SpaceX's simultaneous inclusion in the CRSP and FTSE Russell indices forced billions of dollars in mandatory passive fund buying in a single trading session.[6]

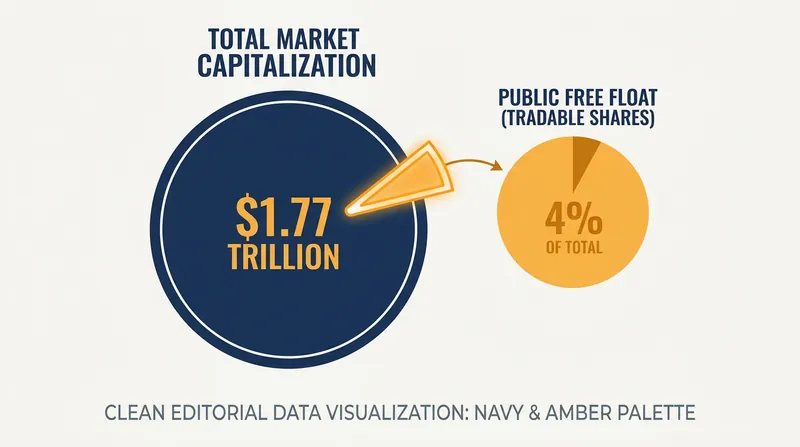

The impact of this forced buying is severely magnified by SpaceX's tiny "free float." Despite its massive overall valuation, the company only made about 4% to 5% of its total shares available to the public during the IPO, keeping the vast majority locked up with insiders and early investors.[2]

When tens of billions of dollars in mandatory buy orders chase a tightly constrained supply of tradable shares, the laws of economics dictate extreme price volatility. To compensate for this imbalance, Nasdaq even applied a unique multiplier to SpaceX's float weight, allowing the stock to count for up to three times its actual tradable value within the index.[3]

Yet, amid the rush to accommodate the aerospace giant, one major holdout remains: the S&P 500. S&P Global, the gatekeeper of the world's most famous stock benchmark, explicitly refused to bend its rules for SpaceX.[3][5]

Following a market consultation, S&P maintained its strict requirement that companies must trade publicly for 12 months and report four consecutive quarters of GAAP profitability before joining the S&P 500. Because SpaceX posted a $4.94 billion net loss in 2025 as it built out its orbital infrastructure, the company remains firmly locked out.[2][5]

This regulatory stubbornness creates a stark divergence in the passive investing landscape. Retail investors holding Vanguard's Total Stock Market ETF—which tracks the CRSP index—now automatically own a slice of SpaceX. Meanwhile, investors holding standard S&P 500 index funds will have zero exposure to the company until at least June 2027.[5]

For everyday investors, the SpaceX IPO serves as a masterclass in modern market plumbing. It highlights how structural mechanics and index rulebooks can dictate a stock's early trading behavior just as much as revenue growth or product announcements.[6]

What to know

- SpaceX debuted on the Nasdaq with a record-breaking $1.77 trillion valuation, floating just 4% to 5% of its total shares.

- Major index providers like Nasdaq and FTSE Russell rewrote their rules to allow SpaceX 'Fast Entry' into their benchmarks.

- Index inclusion forces passive mutual funds and ETFs to automatically buy the stock, creating billions in price-insensitive demand.

- S&P Global refused to alter its rules, meaning S&P 500 index funds will not hold SpaceX until at least mid-2027.

Where opinion splits

Passive Index Providers

Advocates for fast-tracking mega-cap IPOs into market benchmarks.

Index providers like Nasdaq, CRSP, and FTSE Russell argue that their primary mandate is to accurately reflect the broader economy. When a company debuts with a $1.77 trillion valuation, excluding it from a 'total market' index makes the benchmark fundamentally inaccurate. By rewriting their rules to allow 'Fast Entry' after just 5 to 15 trading days, these providers ensure that passive investors immediately capture the growth and market weight of generation-defining companies, rather than waiting months on the sidelines.

Traditional Benchmark Defenders

Proponents of strict seasoning and profitability rules for index inclusion.

Gatekeepers like S&P Global maintain that index inclusion is a mark of stability, not just size. They argue that waiving the standard 12-month seasoning period or the requirement for GAAP profitability exposes passive investors to the extreme volatility and price discovery risks inherent in newly public companies. By forcing SpaceX to wait until at least 2027, S&P prioritizes the long-term reliability of the S&P 500 over the immediate inclusion of the market's newest heavyweight.

Market Structure Analysts

Experts focused on the mechanical plumbing of stock market liquidity.

Market structure analysts emphasize the mechanical risks of fast-tracking low-float companies. When SpaceX floated only 4% to 5% of its shares, it created a severe supply bottleneck. Analysts point out that forcing billions of dollars in passive ETF buying into this tiny pool of available shares artificially inflates the stock price, divorcing it from fundamental valuation metrics. They view the SpaceX IPO as a stress test for modern market plumbing, highlighting the friction between passive investing mandates and actual market liquidity.

Key terms

- Index Inclusion

- The process by which a stock is added to a market benchmark, forcing passive mutual funds and ETFs that track the index to buy the stock.

- Free Float

- The portion of a company's shares that are actively available for trading by the public, excluding restricted shares held by insiders.

- Passive Fund

- An investment vehicle, like an ETF, that automatically tracks a market index rather than relying on a human manager to pick stocks.

- GAAP Profitability

- A measure of a company's earnings calculated using Generally Accepted Accounting Principles, a strict standard required by some index providers.

- Market Capitalization

- The total dollar value of a company's outstanding shares, calculated by multiplying the stock price by the total number of shares.

Unanswered questions

- How the massive influx of passive capital will affect SpaceX's long-term price stability once the initial lock-up periods expire.

- Whether S&P Global will face pressure from institutional investors to eventually relax its entry rules for future mega-cap IPOs.

Reader questions

Why did SpaceX go public?

SpaceX raised $75 billion in its June 2026 IPO to fund its long-term ambitions, including building orbital AI infrastructure and data centers in space.

Can I buy SpaceX stock in my S&P 500 index fund?

Not yet. S&P Global requires companies to be publicly traded for 12 months and report GAAP profitability, meaning SpaceX won't be eligible until at least mid-2027.

What is a free float?

A stock's free float refers to the percentage of total shares that are actually available for the public to trade, excluding locked-up shares held by insiders and early investors.

Why do index funds have to buy SpaceX?

Passive index funds are designed to perfectly replicate a specific market benchmark. If an index provider adds SpaceX, the funds must buy the stock to match the index's new composition.

Sources

Source coverage

6 outlets

3 viewpoints surfaced

[1]MarketWatchMarket Structure Analysts

The initial SpaceX frenzy is cooling off — but a new wave of cash is waiting to strike

Read on MarketWatch →[2]WikipediaTraditional Benchmark Defenders

Initial public offering of SpaceX

Read on Wikipedia →[3]CME GroupPassive Index Providers

The SpaceX Mega-IPO: Why Index Choice Matters

Read on CME Group →[4]MorningstarMarket Structure Analysts

SPCX Stock Price Quote

Read on Morningstar →[5]BloombergTraditional Benchmark Defenders

SpaceX, Other Mega IPOs Denied Fast Index Entry by S&P

Read on Bloomberg →[6]Factlen Editorial TeamMarket Structure Analysts

Synthesis by Factlen editorial team

Read on Factlen Editorial Team →

Comments

Every angle. Every day.

Get finance stories with full source coverage and perspective breakdowns delivered to your inbox.