Memory Stocks Are Having Their Best Year Ever. Why Do They Still Look So Cheap?

Despite record revenues driven by the artificial intelligence boom, memory chipmakers are trading at steep discounts compared to their logic-chip peers. The disconnect highlights a fundamental debate over whether AI has permanently changed the notoriously cyclical semiconductor market.

By Factlen Editorial Team

- Value Investors

- Argue that the massive discount in memory stock valuations provides a wide margin of safety and a cheap entry point into the AI boom.

- AI Hardware Analysts

- Contend that HBM is a specialized, high-margin product that breaks the historical commodity cycle, justifying long-term growth.

- Cyclical Skeptics

- Believe the current profits are a temporary peak and fear that massive capital expenditures will inevitably lead to a supply glut and price crash.

What's not represented

- · Retail consumers facing higher prices for traditional electronics due to memory supply constraints.

- · Environmental advocates monitoring the massive energy and water usage required for new memory fabrication plants.

Why this matters

Understanding the valuation gap in the semiconductor industry offers retail investors a clearer view of where the AI infrastructure build-out is heading next. It reveals how structural bottlenecks in hardware manufacturing create distinct, often overlooked investment opportunities outside of the most famous tech giants.

Key points

- Memory chipmakers are seeing record profits due to the AI boom but trade at steep discounts to logic chip designers.

- AI requires High Bandwidth Memory (HBM) to overcome the 'Memory Wall' and feed data to processors fast enough.

- Manufacturing HBM is resource-intensive, consuming more factory capacity and tightening the overall global memory supply.

- Investors are pricing memory stocks cheaply out of fear that the industry's historical boom-and-bust cycle will repeat.

- Bulls argue that HBM's specialized nature and long-term cloud contracts have fundamentally changed the industry's economics.

The artificial intelligence revolution has minted a new class of trillion-dollar titans, with companies designing the logic processors that train large language models capturing the lion's share of public attention and investor capital. Yet, behind every cutting-edge graphics processing unit (GPU) lies an unsung hero that actually makes the math possible: memory. Without vast pools of hyper-fast memory to store and feed data into the processors, the most advanced AI chips in the world would sit idle, waiting for information to arrive.[4][6]

This critical dependency has led to an unprecedented financial windfall for the companies that manufacture memory chips. According to recent market analyses, memory stocks are currently enjoying their most profitable year on record, driven by insatiable demand from hyperscale cloud providers building out massive AI datacenters. However, a glaring paradox has emerged in the financial markets: despite these record-breaking revenues, the companies producing these essential components look remarkably cheap by historical valuation metrics.[1][6]

The valuation gap is stark. While the designers of logic chips frequently trade at 35 to 40 times their projected forward earnings, the primary manufacturers of memory chips are trading at multiples closer to 10 or 12. This discrepancy has left many analysts and retail investors scratching their heads, wondering if some of the AI boom's biggest earners have quietly become its most attractive bargains.[1]

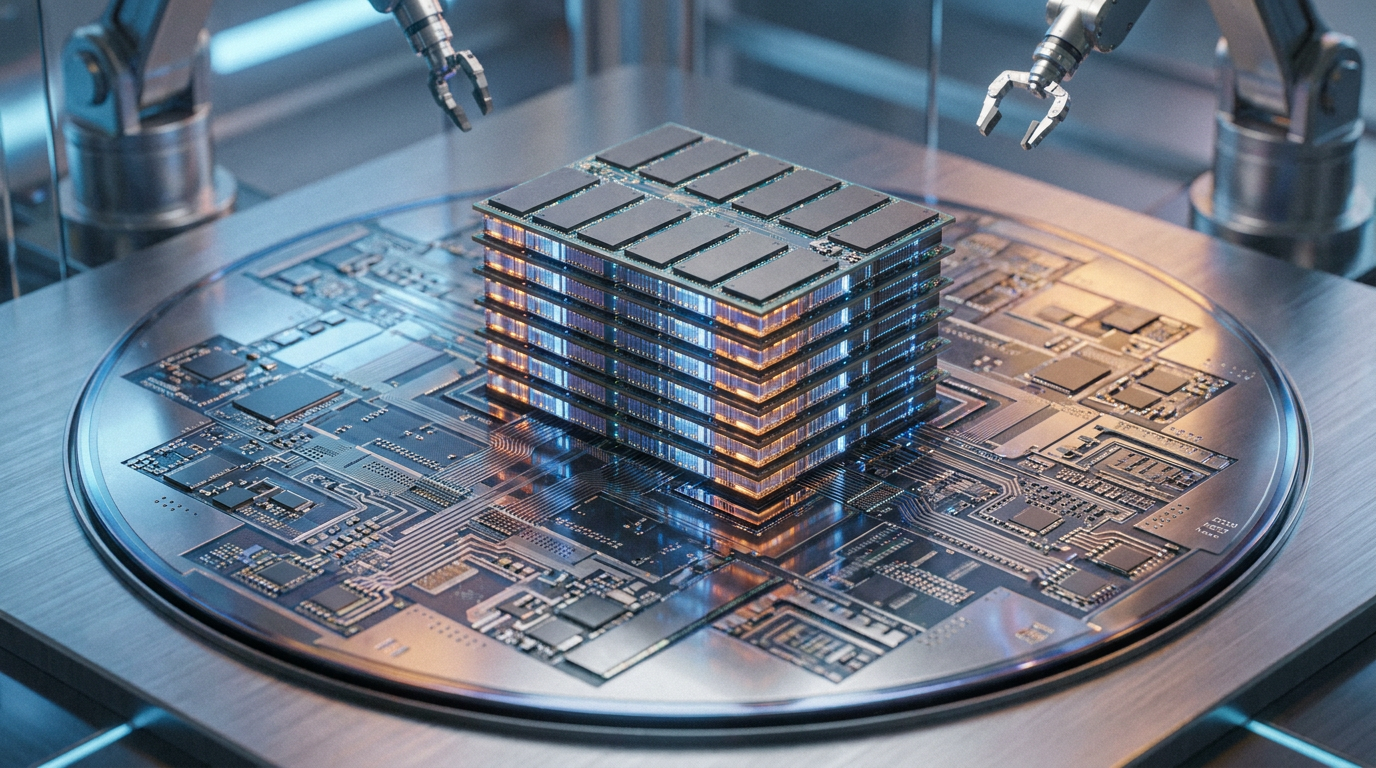

To understand why this gap exists, one must first understand the specific type of memory powering the AI boom: High Bandwidth Memory, or HBM. Traditional computer memory, known as DRAM, is typically placed on a motherboard at a slight distance from the main processor. For decades, this setup worked perfectly well for personal computers and standard servers. But AI workloads require moving unimaginably large datasets simultaneously, exposing a physical limitation known in computer science as the "Memory Wall."[4][6]

The Memory Wall dictates that processors have historically gotten faster at a much quicker rate than the memory bandwidth required to feed them. If a processor can perform a trillion calculations a second, but the memory can only deliver data for a billion, the processor's speed is effectively wasted. HBM solves this physics problem through a marvel of modern engineering: stacking multiple memory chips vertically on top of one another and placing them directly adjacent to the GPU on the same silicon package.[4]

This vertical stacking drastically shortens the distance data must travel and widens the "highway" it travels on, allowing AI models to ingest data at the speeds required for complex training and real-time inference. However, manufacturing HBM is incredibly difficult. It requires microscopic precision to align thousands of vertical connections, known as through-silicon vias, between the stacked layers. The yield rates—the percentage of chips that come off the line functioning perfectly—are significantly lower than those of traditional memory.[2][4]

It requires microscopic precision to align thousands of vertical connections, known as through-silicon vias, between the stacked layers.

Furthermore, HBM is highly resource-intensive to produce. Industry data indicates that manufacturing a single HBM chip consumes roughly three times the silicon wafer capacity of a standard DRAM chip. This structural reality has profound implications for the broader memory market. Because the world's top memory manufacturers are dedicating so much of their factory floor space to lucrative HBM production, the overall supply of traditional memory for smartphones, laptops, and standard servers has tightened considerably.[2][5]

This supply constraint has created a rising tide that is lifting all boats in the memory sector. With traditional memory in shorter supply, prices across the board have stabilized and risen. Recent financial filings from major manufacturers confirm that this dynamic is driving massive margin expansion, as companies enjoy pricing power in both the cutting-edge AI memory segment and the legacy consumer electronics segment.[5]

So, if the technology is indispensable, the margins are expanding, and the supply is structurally constrained, why are the stocks trading at such a discount? The answer lies in the market's long memory of the "semiconductor cycle." Historically, memory has been a highly commoditized, boom-and-bust industry. When prices are high, companies use their windfall profits to build massive new fabrication plants. When those plants come online a few years later, the market floods with supply, prices crash, and profits evaporate.[1][6]

Investors who have been burned by this cycle in the past are inherently skeptical of peak earnings. The current low price-to-earnings ratios reflect a widespread market assumption that the current boom is temporary. Many institutional investors are pricing in a severe cyclical downturn arriving by 2027 or 2028, assuming that the billions of dollars currently being poured into new capital expenditures will inevitably lead to an oversupply of HBM and traditional DRAM.[3][6]

However, a growing chorus of AI hardware analysts argues that this time truly is different. They contend that HBM is not a commodity in the way traditional memory was. Because HBM requires deep co-design and integration with the logic chip designers, it functions more like a custom, high-margin specialty product. The companies producing it are locked into long-term, non-cancellable contracts with cloud providers, providing a level of revenue visibility that the memory industry has never historically enjoyed.[2][3]

Moreover, the memory industry has consolidated into a tight oligopoly. Today, only three companies in the world—SK Hynix, Samsung, and Micron—possess the technological capability and scale to produce HBM in meaningful volumes. This consolidation theoretically reduces the risk of reckless over-expansion, as the three players are highly disciplined and focused on maintaining profitability rather than merely chasing market share at any cost.[2][5]

Value investors are increasingly drawn to this setup. They argue that even if a mild cyclical correction occurs, the downside is already priced into the single-digit multiples. If the AI infrastructure build-out continues at its current pace, driven by the transition from training models to running them continuously for billions of users (inference), the demand for memory will remain structurally elevated for the next decade.[1][6]

Ultimately, the valuation of memory stocks serves as a real-time barometer for the market's confidence in the longevity of the AI boom. If the skeptics are right, the current profits are a cyclical mirage. But if the optimists are correct, and the "Memory Wall" dictates that AI's future depends entirely on advanced memory architectures, these companies may indeed be the most compelling hidden bargains of the technological era.[1][6]

How we got here

Late 2022

The launch of ChatGPT triggers a massive arms race among cloud providers to build AI datacenters, spiking demand for advanced GPUs.

2024

High Bandwidth Memory (HBM) becomes the critical bottleneck in AI server production, prompting memory makers to pivot factory capacity.

2025

Major memory manufacturers report record-breaking revenues and expanding profit margins as HBM commands premium pricing.

Mid-2026

A stark valuation disconnect solidifies, with memory stocks trading at near single-digit multiples despite unprecedented industry growth.

Viewpoints in depth

Value Investors

Focus on the wide margin of safety provided by low valuations in a highly profitable sector.

Value investors look at the memory sector and see a classic mispricing. They argue that the market is overly traumatized by past semiconductor cycles and is failing to recognize the structural shift caused by AI. With forward P/E ratios hovering near 10, they believe the downside risk is already fully priced into the stocks. Even if a mild oversupply occurs in traditional memory, the locked-in, high-margin contracts for HBM provide a revenue floor that didn't exist in previous cycles. For these investors, memory stocks represent the most rational, low-risk entry point into the AI infrastructure trade.

Cyclical Skeptics

Warn that the laws of supply and demand have not been repealed, and a bust is inevitable.

Skeptics point to the billions of dollars currently being deployed in capital expenditures by Samsung, SK Hynix, and Micron to build new fabrication plants. Historically, whenever the memory oligopoly has aggressively expanded capacity simultaneously, it has ended in a supply glut. These analysts argue that while AI demand is real, the hardware build-out is currently in a 'pull-forward' phase, where cloud providers are double-ordering to secure supply. Once these massive new factories come online in 2027 and 2028, skeptics believe the market will flood with chips, collapsing margins and vindicating the current low stock valuations.

AI Hardware Analysts

Argue that HBM is a paradigm shift that transitions memory from a commodity to a custom specialty product.

Hardware specialists emphasize that analyzing HBM through the lens of traditional DRAM is a fundamental mistake. Because HBM must be intricately co-packaged with the GPU, it requires deep, multi-year engineering collaboration between the memory maker and the logic designer (like Nvidia or AMD). This transforms memory from a plug-and-play commodity into a bespoke, high-value component. Furthermore, as AI models transition from being trained in centralized datacenters to running inference on local devices, these analysts project that the sheer volume of memory required globally will permanently elevate the baseline demand, breaking the historical boom-and-bust cycle.

What we don't know

- Whether the current pace of hyperscale cloud datacenter spending will plateau in the next 24 months.

- How quickly next-generation AI models will learn to operate more efficiently, potentially reducing their massive memory requirements.

- If geopolitical tensions could disrupt the highly concentrated supply chains required to manufacture advanced memory packaging.

Key terms

- Forward P/E Ratio

- A valuation metric that divides a company's current stock price by its estimated future earnings per share, used to determine if a stock is over or undervalued.

- The Memory Wall

- A computing bottleneck where the speed of a processor outpaces the speed at which memory can deliver data to it, limiting overall performance.

- Semiconductor Cycle

- The historical boom-and-bust pattern in the chip industry, where high demand leads to over-investment in factories, eventually causing an oversupply and crashing prices.

- Logic Chips

- Processors, like CPUs and GPUs, that perform the actual calculations and "thinking" in a computer, distinct from memory chips which store the data.

Frequently asked

What is High Bandwidth Memory (HBM)?

HBM is a specialized type of computer memory that stacks chips vertically to drastically increase the speed and volume of data sent to a processor, which is essential for AI calculations.

Why are memory stocks considered cheap?

Despite having record-breaking revenue years, memory companies trade at much lower price-to-earnings multiples (around 10-12x) compared to logic chip designers (35-40x) because investors fear a future cyclical downturn.

Who manufactures HBM chips?

The market is a tight oligopoly dominated by three major players: SK Hynix, Samsung, and Micron Technology.

Sources

Source coverage

6 outlets

3 viewpoints surfaced

[1]MarketWatchValue Investors

Memory stocks are having their best year ever. Why do they still look so cheap?

Read on MarketWatch →[2]Financial TimesAI Hardware Analysts

The AI memory bottleneck: Why chipmakers are racing to expand HBM capacity

Read on Financial Times →[3]BloombergCyclical Skeptics

Memory Chip Capex Surges as AI Demand Outstrips Supply

Read on Bloomberg →[4]IEEE SpectrumAI Hardware Analysts

Breaking the Memory Wall: High Bandwidth Memory in Next-Gen AI Accelerators

Read on IEEE Spectrum →[5]U.S. Securities and Exchange CommissionAI Hardware Analysts

Micron Technology Inc. Form 10-Q and Forward Guidance

Read on U.S. Securities and Exchange Commission →[6]Factlen Editorial TeamAI Hardware Analysts

Synthesis by Factlen editorial team

Read on Factlen Editorial Team →

More in finance

See all 5 stories →Retirement Strategy

The Late-Career Roth Pivot: Why Workers Over 50 Are Rethinking Their 401(k) Strategy

6 sources

Stablecoin Adoption

Mastercard and Visa Expand Stablecoin Settlement as Digital Dollars Enter Mainstream Banking

6 sources

Semiconductor Boom

Memory Chip Stocks Hit $1 Trillion Valuations, Yet Remain the AI Boom's Biggest Bargain

7 sources

Every angle. Every day.

Get finance stories with full source coverage and perspective breakdowns delivered to your inbox.