The Mechanics of Mortgage Privacy: How the Homebuyers Privacy Protection Act Ends 'Trigger Leads'

A new federal law bans credit bureaus from selling consumer data to competing lenders during the mortgage application process, ending the barrage of unsolicited calls.

By Factlen Editorial Team

- Consumer Privacy Advocates

- Argue that trigger leads are an invasive, predatory practice that confuses consumers and facilitates bait-and-switch scams.

- Independent Mortgage Brokers

- Argue that the ability to purchase leads fosters vital market competition and prevents massive retail banks from monopolizing the lending industry.

- Traditional Lenders & Trade Groups

- Argue that data syndication destroys the trust between loan officers and clients, unfairly blaming originators for data leaks they cannot control.

What's not represented

- · Telecommunications Providers

- · Lead Generation Call Centers

Why this matters

Applying for a mortgage will no longer result in hundreds of spam calls and texts from unknown brokers. The new law restores control over your personal financial data, allowing you to shop for a home loan in peace.

Key points

- The Homebuyers Privacy Protection Act bans credit bureaus from selling your data when you apply for a mortgage.

- The practice, known as 'trigger leads,' previously resulted in consumers receiving dozens of spam calls a day.

- Exceptions exist if you already have an active account with a financial institution.

- Consumers can still explicitly opt-in if they want their data shared with competing lenders.

- Without automated offers, homebuyers must now proactively shop around to secure the best interest rates.

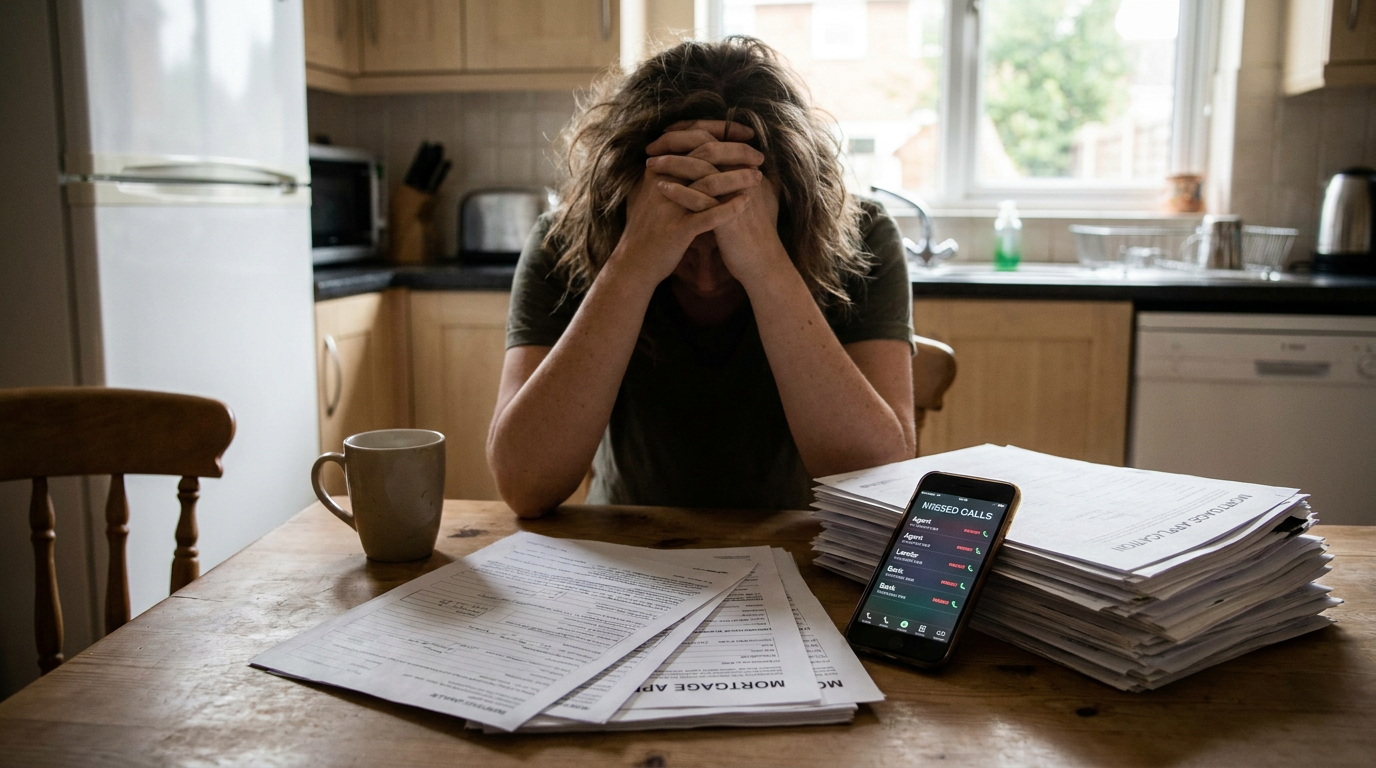

For decades, applying for a mortgage triggered an immediate, overwhelming, and deeply frustrating side effect for American consumers: a relentless barrage of unsolicited phone calls. Within minutes of a loan officer pulling a prospective buyer's credit report to begin the pre-approval process, the consumer's phone would begin to ring, often dozens of times a day, accompanied by a flood of text messages and emails. This phenomenon was not a coincidence, nor was it the result of a malicious data breach. It was the direct result of a highly lucrative, perfectly legal data-brokerage practice known within the financial industry as "trigger leads." Credit reporting agencies actively monitored their systems for hard credit inquiries related to mortgages and instantly sold that real-time data to competing lenders, turning a private financial milestone into a public auction.[4][6]

Now, the landscape of real estate financing is undergoing a fundamental privacy shift that promises to restore peace to the homebuying process. The Homebuyers Privacy Protection Act (HPPA) has officially dismantled the trigger lead ecosystem, fundamentally altering how consumer mortgage data is commodified. By amending the Fair Credit Reporting Act, the new legislation strictly prohibits credit bureaus from selling a consumer's contact information to third-party lenders simply because they applied for a home loan. This legislative overhaul represents a massive victory for consumer privacy advocates and traditional lenders alike, effectively starving the automated dialers of their fuel and restoring a much-needed barrier of privacy around one of the most significant financial transactions of a person's life.[1][3]

To truly understand the mechanics of the HPPA, one must first examine the hidden machinery of the trigger lead economy. When a consumer applies for a mortgage, the originating lender must request a comprehensive credit report from one or more of the three major credit bureaus: Equifax, Experian, or TransUnion. This "hard pull" is a highly specific data point; it signals a clear, immediate, and verified intent to borrow hundreds of thousands of dollars. Recognizing the immense commercial value of this intent, the credit bureaus packaged these inquiries into real-time data feeds. For a nominal fee—often ranging from $1 to $5 per individual lead—competing mortgage brokers and lead-generation firms could purchase the contact information of the applicant the exact moment the credit was pulled, allowing them to intercept the transaction.[6]

The practice of selling trigger leads was originally sanctioned under the Fair Credit Reporting Act as a form of "prescreened" offering. The legislative intent back in the 1990s was rooted in the idea of fostering market competition. Regulators theorized that if multiple lenders knew a consumer was actively shopping for a loan, they would naturally compete to offer the lowest possible interest rate and the best closing terms. In a pre-digital era, this might have resulted in a few competitive letters in the mail. However, the modern digital economy, armed with automated predictive dialers and aggressive offshore lead-generation call centers, warped this original intent into a high-speed harassment engine that overwhelmed consumers rather than empowering them.[3][4]

The Consumer Financial Protection Bureau (CFPB) and various state attorneys general noted a massive, sustained surge in complaints related to these aggressive marketing tactics over the past five years. The sheer volume of communication—sometimes exceeding 100 calls within a 24-hour window—often deeply confused and distressed applicants. Many consumers mistakenly believed the callers were affiliated with their chosen lender or that their identity had been stolen. This confusion created a fertile ground for bait-and-switch scenarios, where unscrupulous brokers would promise unrealistically low rates over the phone just to derail the original application, ultimately trapping the consumer in a less favorable financial product once the closing date approached.[4]

The Homebuyers Privacy Protection Act rewrites the rules of engagement by explicitly prohibiting credit reporting agencies from furnishing these trigger leads to unaffiliated third parties. The mechanism of the ban is straightforward but devastating to the lead-generation industry: the sale of an applicant's data based solely on a mortgage credit inquiry is now a violation of federal law. This effectively ends the practice of "buying the borrower" out from under the originating loan officer. The legislation was heavily championed by the Mortgage Bankers Association (MBA), which argued that trigger leads fundamentally damaged the trust between loan officers and their clients. When a client's phone exploded with spam immediately after a consultation, the originating loan officer often unfairly took the blame for a "data leak" they had absolutely no control over.[1][5]

While the ban is comprehensive, the legislation does carve out specific, highly regulated exceptions to ensure that legitimate, pre-existing financial relationships are not disrupted by the new privacy shield. If a consumer already has an active account with a financial institution—such as a checking account, an auto loan, or an existing mortgage—that specific institution may still be notified of the new credit pull. This allows a consumer's primary bank to offer competitive rates to retain their business. Furthermore, consumers retain the absolute right to explicitly opt-in to third-party offers. If a homebuyer actively wants to broadcast their application to the open market to solicit competing bids, they can authorize the credit bureau to syndicate their data. The critical, paradigm-shifting difference is moving the entire system from a default "opt-out" to a strict "opt-in."[3][6]

This allows a consumer's primary bank to offer competitive rates to retain their business.

The implementation of the HPPA forces a significant strategic pivot for independent, direct-to-consumer mortgage brokers and online lending platforms. For years, purchasing trigger leads was a primary, highly efficient customer acquisition strategy for smaller shops that lacked the massive, multi-million-dollar marketing budgets of retail banking giants. By buying leads, a small brokerage in Ohio could instantly compete for a borrower in Florida the moment they entered the market. Without the ability to intercept these active shoppers, independent brokers must now invest heavily in organic marketing, search engine optimization, and building traditional referral networks with local real estate agents. Industry analysts expect the cost of customer acquisition to rise significantly across the sector as the cheapest, highest-intent leads vanish from the open market.[2]

For the major credit reporting agencies, the passage of the HPPA represents the abrupt closure of a highly profitable, zero-marginal-cost revenue stream. While the sale of mortgage trigger leads represented only a fraction of total bureau revenue compared to their core credit scoring businesses, the profit margins on these data feeds were exceptionally high. The bureaus were essentially selling the exact same data point to dozens of different buyers simultaneously, generating outsized returns on a single credit inquiry. The loss of this revenue highlights a broader regulatory trend of scrutinizing and restricting how consumer data is monetized by the institutions entrusted to safeguard it, signaling potential future crackdowns on other forms of prescreened data sales.[6]

Ultimately, while the HPPA provides immense relief from predatory marketing, it also places the burden of comparison shopping squarely back onto the shoulders of the consumer. Without a flood of unsolicited offers arriving by phone and email, homebuyers must proactively seek out multiple quotes to ensure they are securing the best possible interest rate. Financial advisors emphasize that the elimination of trigger leads is a massive victory for consumer privacy, but it should not lead to financial complacency. The original premise of the trigger lead—that competition lowers rates—remains mathematically true. Consumers are now urged to manually apply with at least three different lenders—a local bank, a credit union, and an online broker—within the standard 45-day credit shopping window to replicate the benefits of competition without the harassment.[6]

The journey to passing the HPPA was marked by intense lobbying and a rare display of bipartisan consensus. Lawmakers from across the political spectrum found common ground in their shared disdain for the aggressive telemarketing tactics that plagued their constituents. Testimonies during congressional hearings painted a grim picture of the trigger lead ecosystem, featuring stories of elderly homebuyers being harassed to the point of tears and veterans being targeted by predatory lenders offering deceptive VA loan refinancing schemes. The unified front presented by consumer advocacy groups and traditional banking lobbies proved too powerful for the data brokerage industry to overcome, culminating in a sweeping legislative victory that prioritized peace of mind over data monetization.[3][5]

Prior to the enactment of the HPPA, consumers and telecommunications companies were locked in a perpetual technological arms race against lead-generation firms. Carriers deployed increasingly sophisticated spam-blocking algorithms, while consumers relied on third-party apps to filter unknown numbers. However, the lead buyers constantly adapted, utilizing localized spoofing techniques to make their calls appear as though they were originating from the consumer's own area code or even from the very bank they had just visited. This technological cat-and-mouse game was ultimately a losing battle for the consumer, as the sheer volume of calls inevitably overwhelmed even the most robust digital defenses. The legislative ban cuts the problem off at the source, rendering these evasive calling tactics obsolete in the mortgage sector.[4][6]

The elimination of trigger leads is particularly impactful for first-time homebuyers, who are often the most vulnerable to the confusion and stress of the mortgage process. Navigating interest rates, closing costs, and escrow accounts is daunting enough without the added pressure of high-pressure sales tactics from unknown entities. First-time buyers were frequently the primary targets of bait-and-switch schemes, as they lacked the experience to identify unrealistic loan estimates. By securing the application process, the HPPA allows these new entrants to the housing market to work closely with their chosen loan officers, ask questions without fear of triggering a data avalanche, and make complex financial decisions in a secure, low-pressure environment.[4]

The enforcement mechanisms embedded within the Homebuyers Privacy Protection Act are designed to ensure strict compliance from the credit reporting agencies. The Consumer Financial Protection Bureau has been granted expanded authority to audit the data sales practices of the major bureaus and levy substantial fines for any unauthorized distribution of mortgage inquiry data. Furthermore, the legislation empowers state attorneys general to pursue legal action against both the data furnishers and the entities purchasing illegal leads. This multi-layered enforcement approach is intended to create a powerful deterrent, ensuring that the lucrative nature of trigger leads does not tempt industry players to find loopholes or alternative methods of syndicating consumer intent.[3][4]

By restoring control over personal financial data, the Homebuyers Privacy Protection Act transforms the mortgage application from a chaotic public broadcast back into a secure, private transaction. It represents a rare and definitive legislative moment where consumer privacy triumphed over entrenched data commodification. As the housing market adapts to this new reality, the focus will shift back to relationship-based lending and proactive consumer education, ensuring that the path to homeownership is defined by informed choices rather than aggressive telemarketing.[1][6]

How we got here

1990s

FCRA amendments allow for prescreened credit offers, laying the groundwork for the trigger lead industry.

2021-2023

Digital automation causes a massive spike in trigger lead volume, leading to widespread consumer harassment.

Late 2023

The Homebuyers Privacy Protection Act is formally introduced in Congress with bipartisan support.

2024-2025

Major trade groups like the MBA heavily lobby for the bill's passage amid rising CFPB complaints.

2026

The HPPA is signed into law, officially banning the unauthorized sale of mortgage trigger leads.

Viewpoints in depth

Consumer Privacy Advocates

Argue that trigger leads are an invasive, predatory practice that confuses consumers and facilitates bait-and-switch scams.

Consumer watchdogs and the CFPB have long maintained that the trigger lead ecosystem fundamentally exploits the homebuyer. They argue that the sheer volume of calls—often utilizing spoofed local numbers—creates an environment of panic and confusion rather than healthy competition. By eliminating this practice, advocates believe the mortgage process becomes significantly safer, particularly for first-time buyers who are most susceptible to high-pressure sales tactics and deceptive loan estimates.

Independent Mortgage Brokers

Argue that the ability to purchase leads fosters vital market competition and prevents massive retail banks from monopolizing the lending industry.

For smaller, independent brokerage firms, trigger leads were a great equalizer. These brokers argue that by purchasing real-time data, they could intercept consumers who might otherwise default to their massive retail bank, offering them significantly lower rates and better service. They warn that banning the practice entirely will drive up customer acquisition costs, forcing smaller players out of the market and ultimately leaving consumers with fewer choices and potentially higher interest rates in the long run.

Traditional Lenders & Trade Groups

Argue that data syndication destroys the trust between loan officers and clients, unfairly blaming originators for data leaks they cannot control.

Organizations like the Mortgage Bankers Association strongly supported the ban because trigger leads actively undermined their members' relationships with clients. When a consumer sat down with a loan officer, pulled their credit, and immediately received 50 spam calls, the consumer naturally assumed the loan officer had sold their data. Traditional lenders argue that the HPPA restores the integrity of the application process, allowing them to advise clients without the constant interference of aggressive third-party telemarketers.

What we don't know

- How significantly customer acquisition costs will rise for independent mortgage brokers without access to trigger leads.

- Whether the credit bureaus will attempt to develop new, legally compliant data products to replace the lost revenue.

- If lawmakers will use the momentum of the HPPA to target similar prescreened data sales in the auto loan and credit card industries.

Key terms

- Trigger Lead

- A data product sold by credit bureaus containing the contact information of a consumer who just applied for a mortgage.

- Hard Pull

- A comprehensive credit inquiry initiated by a lender that temporarily impacts a consumer's credit score and signals intent to borrow.

- Prescreened Offer

- A firm offer of credit extended to a consumer based on data purchased from a credit reporting agency.

- Bait-and-Switch

- A deceptive sales tactic where a broker offers an unrealistically low rate to win business, only to change the terms later.

Frequently asked

Will my phone still ring if I apply for a mortgage today?

No. Under the new law, credit bureaus cannot sell your application data to third parties, drastically reducing unsolicited calls.

Can my current bank still contact me if I apply elsewhere?

Yes. The law includes an exception allowing institutions where you have an existing active account to offer you competing rates.

How do I make sure I get the best rate without trigger leads?

You must proactively apply with multiple lenders—such as a local bank, a credit union, and an online broker—within a 45-day window to compare offers manually.

Does this law apply to auto loans or credit cards?

No. The Homebuyers Privacy Protection Act specifically targets mortgage-related credit inquiries, though regulators are scrutinizing other sectors.

Sources

Source coverage

6 outlets

3 viewpoints surfaced

[1]HousingWireTraditional Lenders & Trade Groups

Senate passes Homebuyers Privacy Protection Act to ban trigger leads

Read on HousingWire →[2]National Mortgage ProfessionalIndependent Mortgage Brokers

Trigger leads officially banned as HPPA signed into law

Read on National Mortgage Professional →[3]Congress.govTraditional Lenders & Trade Groups

S.3502 - Homebuyers Privacy Protection Act

Read on Congress.gov →[4]Consumer Financial Protection BureauConsumer Privacy Advocates

Issue Spotlight: Mortgage Trigger Leads and Consumer Harm

Read on Consumer Financial Protection Bureau →[5]Mortgage Bankers AssociationTraditional Lenders & Trade Groups

MBA Applauds Passage of the Homebuyers Privacy Protection Act

Read on Mortgage Bankers Association →[6]Factlen Editorial TeamConsumer Privacy Advocates

Synthesis by Factlen editorial team

Read on Factlen Editorial Team →

More in finance

See all 5 stories →AI Infrastructure

The Mechanics of AI Infrastructure: How KKR's $10 Billion Fund with Nvidia Reshapes Data Center Investment

7 sources

Crypto Regulation

The Mechanics of Crypto Custody: How the SEC's Rescission of SAB 121 Reshapes Bank Balance Sheets

8 sources

Education Finance

The Mechanics of the 529 Overhaul: How the Doubled K-12 Limit and Expanded Credentialing Reshape Education Savings

7 sources

Every angle. Every day.

Get finance stories with full source coverage and perspective breakdowns delivered to your inbox.